Long PNDORA

Kaili Tu, kailitu2025@u.northwestern.edu

Thesis

In my view, Pandora is a sustainable charms jewelry business whose shares trade at an attractive valuation (P/IV = 0.53). There is an opportunity to buy in while it is still trading so low over inflationary concerns.

After both a strong Q1 and Q2 for Pandora (record double-digit revenue growth), I believe that the impact of inflation on the business is less than what many investors initially expected– gift-giving norms substantiate this. Many Pandora bracelets are given as gifts (~two-thirds of revenue), and the occasions for these gifts such as anniversaries, graduations, birthdays, etc. are special; evidently, customers are happy to spend on these gifts, even in inflationary times. Retail metrics such as basket size and traffic conversion have stayed intact, and management has not seen any softening consumer sentiment. Similar trends are happening within the luxury market, which also has been outperforming investor expectations with regards to inflation.

Pandora Overview

Pandora is a Danish jewelry manufacturer and retailer known for its personalizable charm bracelets. They are not a luxury brand (like LVMH) nor a mass jewelry marketer (like Signet). Instead, they operate in a niche segment of fashionable, affordable jewelry with a loyal customer base (tending to be younger) and a strong, sustainable brand in charms. In my opinion, this creates their competitive advantage.

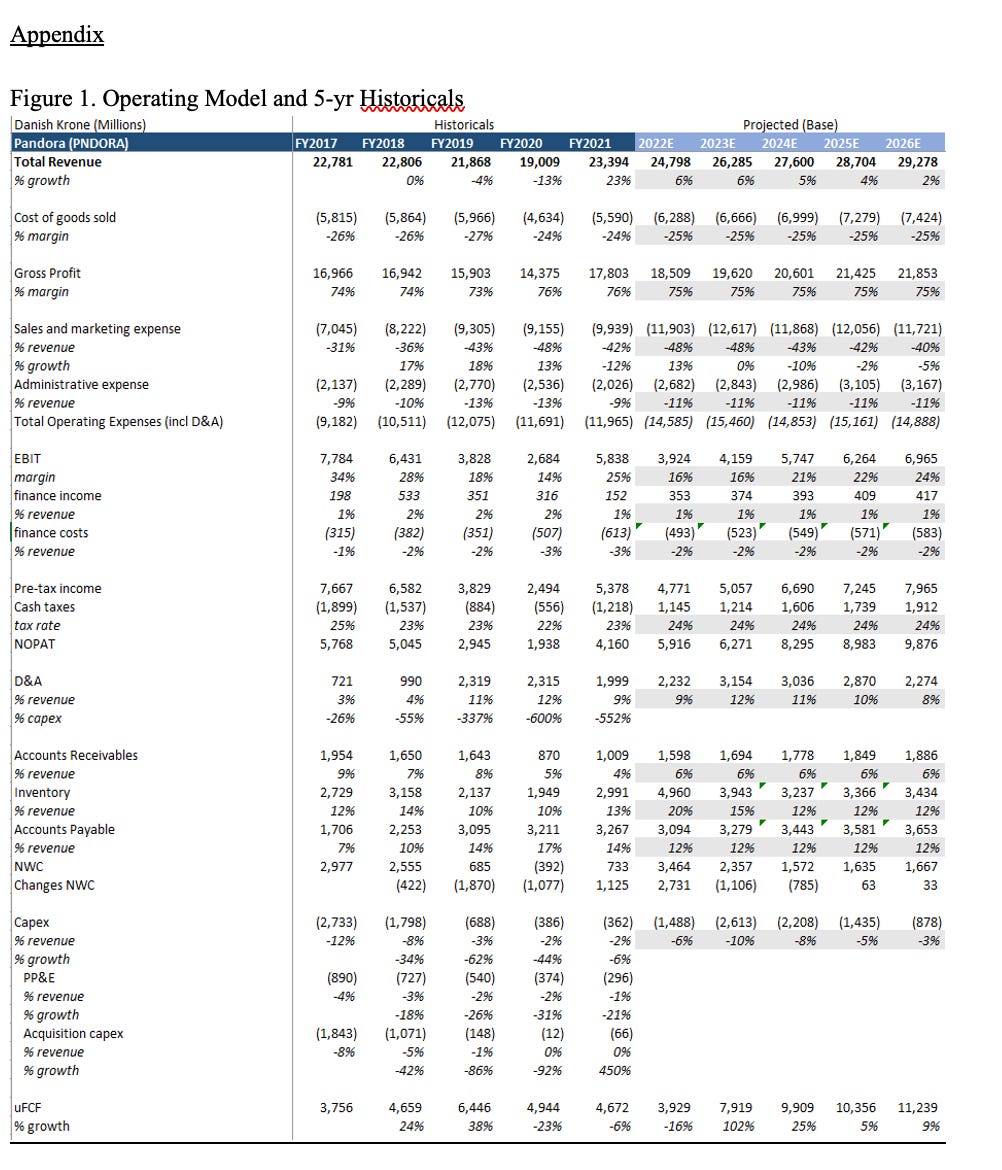

Currently, their Moments and Collabs collection, which makes up their charms collection, is ~70% of revenue. Their Timeless collection, made up of elegant, classic jewelry, is ~17% of revenue. A variety of other segments make up the remainder (Me, their GenZ initiative, is ~3%; Brilliance, their diamond collection, is ~0.2%; Signature, another classic collection, is 9%).

Because so much of their revenue comes from charms (Moments collection), it is essential that in order for Pandora to do well, charms need to remain popular for consumers–and this has proven to be a sustainable business for Pandora over time. Management realizes that their core brand strength lies in selling charms (Moments collection); thus, their initiatives center around supporting their charms collection and producing new products in this category (Disney/Marvel/Harry Potter collaboration charms, Valentines’ special charms, etc.). In addition, their newer, higher margin gold/diamond products in the Brilliance collection are an area where they are increasing investment into (although unlike competitors, they are focusing on a younger demographic of consumers who are “self-gifters”– by selling more affordable, sustainable fashion jewelry).

Marketing is a large portion of Pandora’s core business, with expenses making up around 40% of revenue. In addition to collaborating with other brands like Disney and Marvel, Pandora’s marketing strategy involves targeting younger consumers by partnering with young celebrities like Millie Bobby Brown (Stranger Things actress), Addison Rae (TikTok star), Beabadoobee (indie singer), and more. They also have a small presence on youtube with most videos getting several thousand views (although some new product launches have gained up to 14M+ views, which signals strong GenZ interest in the next generation of Pandora products). Because they have such a high gross margin (~70%), they can market much more than smaller competitors, and they seem to be very successful at doing so.

In terms of geography, revenue is broken down into 35% EMEA (UK, Italy, France, Germany, Denmark), 30% Americas (US), 10% APAC (China, Australia), and 25% Other (Spain, Mexico, Canada, etc.). They see expansion particularly in the US and China. In the US, they are targeting GenZ growth and seem to be seeing success (partnering with young influencers, etc.). In China, management has admitted that branding is shaky since in the past, they had marketed their products more as a full assortment jewelry brand, not just charms bracelets. Thus, there is a disconnect with Chinese consumers, who have many other traditional Chinese jewelry options. Pandora currently operates only ~200 stores in China, which make up merely 5% of revenue. Management is working on investing more marketing into this geographic region once COVID concerns start to ease, which should solidify their branding and encourage more sales (which they have seen happen in other geographies such as the US). Irving Holmes Wong (who used to work with L'oreal, Avon, and Revlon) was just hired as General Manager in China. There is belief that he will be able to successfully connect Pandora to Chinese consumers, which he has done with other western brands in the past.

Finally, based on speaking with customers and employees while visiting stores across the country, it is also apparent that the company has a significant amount of pricing power, which is reflected in their ~70% gross margins. Stickiness is also part of the brand in the sense that many Pandora charm bracelet owners keep on buying Pandora charms as collectibles (70% of business is repeat buying, with charms priced at ~$50+ each). There is a certain sentimentality / personalizable aspect when it comes to the charms, and in fact, about two-thirds of their revenue comes from gift-giving, which encourages this.

Trends

Considering some of their closest luxury competitors in the jewelry space, some industry trends are moving towards 1. more branding (pricing power for established brands, DTC will heat up) 2. more digital and 3. more focus on sustainability.

To touch on branding, Pandora is a direct-to-consumer brand. More than 75% of their transactions are done direct with their customers, and this was a big part of their restructuring initiative during the late 2010s, where they moved from wholesale to DTC– establishing their brand more effectively.

To touch on their online presence, Pandora has a strong online presence as a result of engaging with younger consumers (and they have this advantage over their more luxury counterparts, who do not focus as much on online sales; instead, luxury tends to have a focus on offline, which is why this space got hit hard by COVID). ~30% of sales are already online (with the other percentage of retail sales being ~40% in-stores & ~30% still wholesale), and management sees this percentage growing in the coming years. Furthermore, about 80% of in-store customers start by browsing online then completing the purchase in-stores. In fact, their new concept stores are modeled after the ease of online browsing, which has seen better customer engagement and conversion rates.

To touch on sustainability, their new collection, Brilliance, is their sustainable gold/diamond collection, and they now have their own Lab Credit Diamonds facility in North America (first step in the huge gold and diamond markets). The diamonds are cut and polished using only renewable energy, and it's also the first collection setting 100% recycled silver and gold from Pandora. Along similar veins, when it comes to manufacturing and sourcing, they have their own facility in Thailand, which allows them to manufacture their jewelry at cheaper cost levels than competitors (thus, the quality of their jewelry is harder to replicate at similar cost levels and manufacturing scale).

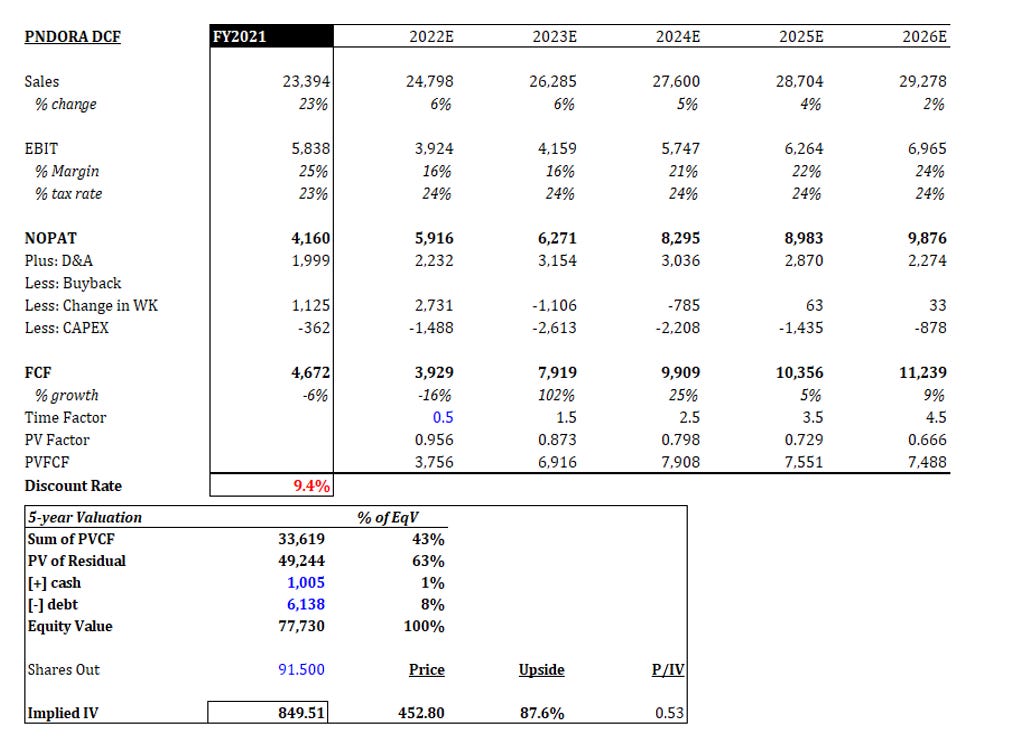

Valuation

My IV estimate for Pandora is DKK 849.51 per share. For my primary assumptions, I aimed to be conservative rather than accurate to the exact unit forecast (since disclosure has been spotty). Currently in the model, I only have sales growing at 6% during 2022-2023 then declining, which they will likely outperform (based on recent performance and sell-side estimates, which are more optimistic than I am). I had EBIT margins declining significantly in the short-term to account for large marketing expenses since they are planning on spending more within the US and China to meet their branding/strategy goals in the next few years. In addition, with the opening of their Lab Credit Diamonds facility, I also expect more CapEx and D&A in the near future, and this will also have a drag on margins.