Long IAC

Nicholas Brown, Harvard Class of '23, nicholas_brown@college.harvard.edu

Summary

IAC is a great business selling substantially below fair value. Dotdash Meredith, its most valuable asset, is much misunderstood. On December 31st, 2021, Dotdash, a fast-growing web publisher (known for Investopedia), acquired Meredith, the largest legacy magazine brand company in the US. I expect Dotdash to reveal the value of Meredith’s mostly print brands.

Although Dotdash Meredith is a category leader with a strong moat and excellent growth trajectory, the market values it well below $600 million. In actuality, it is probably worth ~$3 billion conservatively and could reasonably be justified at a $4-5 billion valuation.

At IAC’s current price, you get Dotdash Meredith (one of the largest and best managed online & print publishers in the US) for free.

IAC Background

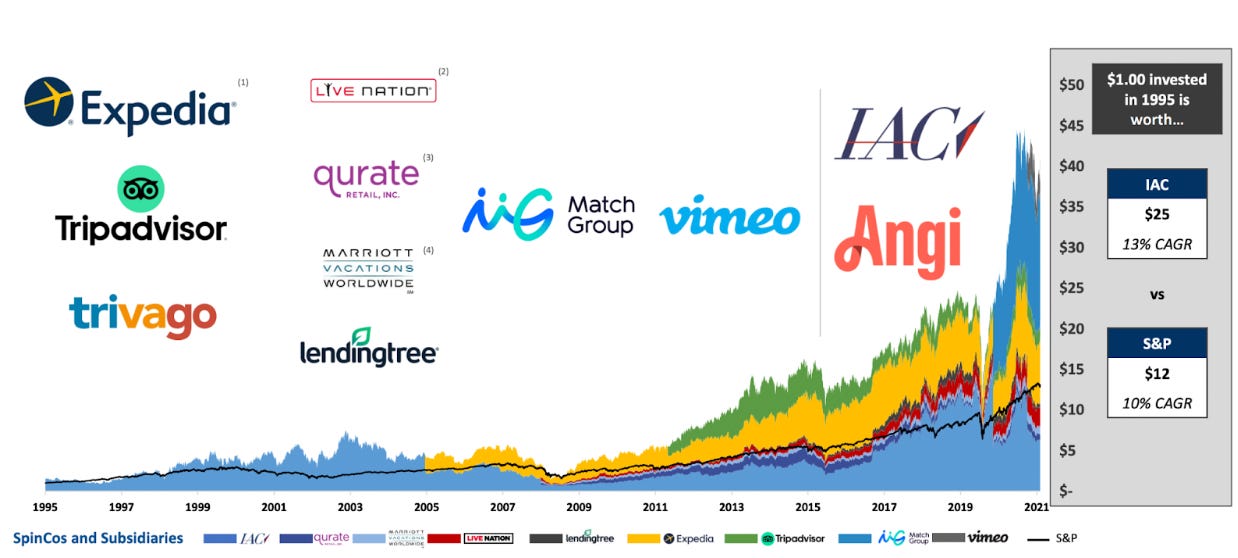

IAC functions like a mini digital Berkshire Hathaway. They are value investors who buy exceptional undervalued, mostly digital companies, grow them through a decentralized manner (like Berkshire), then once mature spin them off to hand value to shareholders (unlike Berkshire). Their past spinoffs include Vimeo, Match Group (Match.com, Tinder, Hinge, OK Cupid, Plenty of Fish), Expedia, TripAdvisor, HSN, LendingTree, Interval Leisure Group, and Live Nation (formerly Ticketmaster).

What IAC Owns

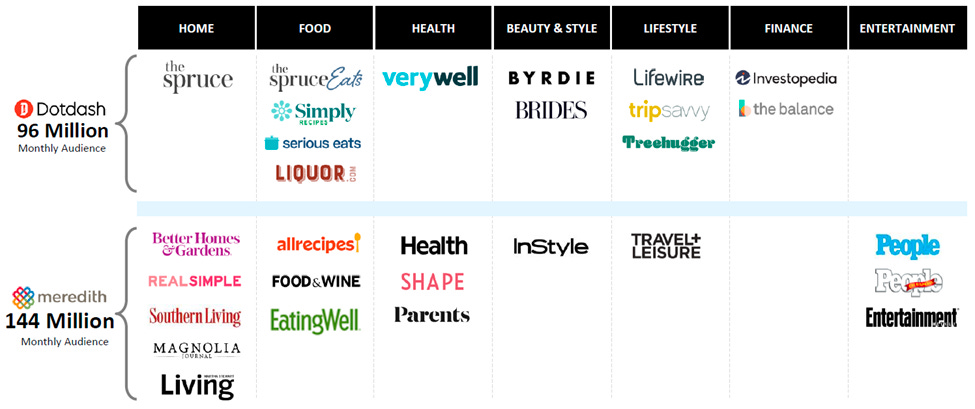

Dotdash Meredith

One of the largest digital and print publishers in America. Formed on December 31st, 2021 when Dotdash bought Meredith for their legacy magazine brands. Having expertise in search engine optimization (SEO), I can say confidently they are the best publisher at SEO in the US and they likely have excellent underlying unit economics. I am interested in IAC mainly to gain exposure to Dotdash Meredith.

27% of Turo and a warrant that can raise the stake to 37%

Turo is Airbnb for cars. It is the leading peer-to-peer carsharing company in America. IAC bought its stake in 2019 for $250 million, making them Turo’s largest shareholder. Turo is my second favorite asset in IAC.

84.5% of Angi (formerly Angie’s List, HomeAdvisor, and Handy)

Currently transitioning to become Uber for home services. I don’t have much confidence in this company’s prospects. I don’t understand how you can price many contractor jobs before it is appraised in person. That said, IAC CEO Joey Levin said in his Q2 2022 shareholder letter that he has high conviction on Angi. Perhaps he sees something I am not seeing. I am fine with Angi going to $0.

16.5% of MGM Resorts International

Dominant casino position on the Las Vegas strip. This is IAC’s attempt to gain exposure to and help produce a leader in online gambling.

Care.com

The world’s leading platform for finding and managing family care. Bought for $500 million after 2019 background check scandal discovered by The Bear Cave. IAC has resolved this issue.

The Daily Beast

Not worth going into as I’m not sure it’s worth much.

Ask applications and Ask Media Group

A set of dying businesses that produce cash for IAC to invest with.

Vivian Health

An app marketplace that connects healthcare professionals, especially nurses, with temporary and permanent jobs. Vivian has 800,000+ registered professionals. Recently did a capital raise with a valuation of $400 million. IAC owns 3/4ths of Vivian Health.

Bluecrew

An app that connects workers with W-2 employment in warehouse, manufacturing, retail, and hospitality. Not currently worth much.

Mosaic Group

A portfolio of 40+ mobile apps that includes popular titles like RoboKiller, iTranslate, and NOAA Weather Radar Live: Clime.

Newco

IAC’s tech incubator. Their prior incubator built Tinder. Newco does not seem to have anything particularly valuable in it but public information on it is scarce.

Shareholder-aligned Ownership Structure

Barry Diller IAC Chairperson owns 8.444%

Joseph Levin IAC CEO owns 5.4672%

IAC’s Remarkable Board

Leaders in Media and Investing with excellent track records

Barry Diller

Former CEO of Fox and Paramount Pictures and IAC founder

Michael Eisner

Former Disney CEO who transformed the company from a film and theme park company with $1.8 billion in enterprise value into a global media empire valued at $80 billion

Alexander von Furstenberg

Founder and CIO of Ranger Global Advisors, a value investing fund. Previously served as Co-Managing Member and CIO of Arrow Capital Management, an investment firm that annualized at 22.4% over an 8-year period. Joined IAC on Jan 2022.

Now let’s get into Dotdash Meredith.

Dotdash Meredith

I developed enormous respect for Dotdash (premerger) in 2020 when I rigorously studied SEO-driven publishers. I came away believing that if I could own any company it would be Dotdash. They are one of if not the best at SEO. Take for example their website The Spruce. Founded in 2017, today it is the single biggest home brand on the internet by search traffic (32 million monthly organic). Keep in mind that winning in Google search is exceedingly difficult without brand recognition and a history of authority, expertise, and trustworthiness. Without the benefits of storied brands, Dotdash rapidly grew from an outsider upstart in 2016 to what I believe to be the most enviable collection of online article websites in the US. They currently reach 95% of U.S. women every month across 40+ brands and are only getting stronger.

Dotdash has a remarkable track record of growing sites that they acquire. Organic traffic growth since acquisition:

Investopedia – 5x in six years

Byrdie – 10.8x in 3.5 years

MyDomaine – 2.5x in 3.5 years

Serious Eats – 2.9x in 2 years

Simple Recipes – 1.5x in 2 years

Brides – 5.2x in 3 years

Liquor.com – 2.4x in 3 years

Tree Hugger – 4x in 2.5 years

I expect Dotdash will repeat this growth with Meredith’s web properties. They have a proven track record of growing mostly unestablished brands. Note that in the SEO world it is much easier to grow a highly recognized brand than to create brands from scratch. Dotdash now has the chance to show what it can do with some of the most highly recognized legacy brands in the US. I expect their future results to be remarkable.

Growth Trajectory

IAC guided for over $450M of pro forma digital adjusted EBITDA by 2023. In Q2 2022 they stated that this would take another year since transferring Meredith’s web properties onto Dotdash’s system was taking longer than expected and due to softness in the macro advertising market.

Dotdash Meredith has provided long-term guidance of 15-20% revenue growth. This appears quite achievable. Prior to the merger, Dotdash's revenue has grown at a CAGR of 32% from 2018 to LTM for the period ending June 30, 2021. I expect Dotdash and Meredith to grow rapidly under Dotdash’s unparalleled stewardship. Meredith has extensive knowledge of the marketing industry and long-standing relationships with advertisers, some going back as far as 50 years. Dotdash Meredith's CEO Neil Vogel has stated that this is why Meredith’s ad rates are twice as high as Dotdash’s. Through merging, Dotdash’s newcomer brands can get the help they need to approach ad rate parity with Meredith’s legacy brands. Additionally, Meredith’s 72,000 square foot physical facilities can help Dotdash and Meredith grow their product review capabilities, which power Dotdash’s fastest-growing source of revenue, affiliate marketing. Dotdash, in turn, can help Meredith’s brands grow their site traffic and expand their product review capabilities, a revenue source with enormous growth potential discussed below.

Expanding Dotdash and Meredith’s product review capabilities is crucial for their long-term growth. Their Affiliate Commerce and Other revenue growth CAGR was ~91% from 2016 to LTM Q3 2019. As Dotdash’s revenue mix has shifted towards Affiliate Commerce and Other (now called Commerce and Performance Marketing), their overall revenue CAGR has grown from around 19% from 2016 through 2019 to 32% from 2018 to LTM for the period ended June 30, 2021. Given Dotdash and Meredith’s synergies (discussed above) and that the faster-growing AC&O segment will likely lap advertising revenue in the next few years, I expect Dotdash Meredith to grow revenue in excess of 20% per year over the next five years.

Dotdash Meredith’s Economics

Besides product-led growth, SEO is arguably the best long-term growth marketing strategy if done exceptionally well. It is a sustainable growth driver that can produce asymmetrical rewards relative to the capital invested. I expect Dotdash Meredith’s content production and article upkeep costs to become relatively small compared to the cash being generated from their already produced high-performing articles. As content spending has become a smaller portion of total revenue, Dotdash’s adjusted EBITDA margins have expanded every year from -21.6% in FY 2016 to 30.96% in FY 2020. FY 2021 adjusted EBITDA fell to 7.36% due to the inclusion of Meredith’s low-margin print business and advertising spending falling on recession fears. I expect margins will trend upwards sometime in the next year and eventually reach 30% and beyond as digital becomes a larger source of the total revenue mix.

Dotdash Meredith’s Moat

Dotdash Meredith’s moat is simple. They understand SEO and how to do efficient high-scale best-in-class content production better than nearly anyone else. This may appear to only be a narrow moat — a slight advantage over competitors — but in SEO this can be enormous. This algorithmic expertise combined with outstanding management and execution explains why Vogel could say “Dotdash is the only growing, profitable, digital publisher I can think of.” Furthermore, having so many sites on the same proprietary content management system and tech stack allows them to efficiently and cheaply make modifications to their websites, spreading the costs between many top-performing websites.

Further, I believe that as Google’s algorithmic standards for ranking at the top of search results progressively become more stringent, intent-driven content publishing will consolidate and new entrants will become less frequent. We are already seeing this with Dotdash consolidating the industry through its acquisitions.

Is Dotdash Meredith at risk of being destroyed by a Google search algorithm update?

I believe that Dotdash Meredith is one of the least risky sets of web properties. I don’t expect any algorithmic crises for Dotdash Meredith in the foreseeable future. Dotdash has developed substantial E-A-T (expertise, authoritativeness, and trustworthiness) signals, well beyond competitors. Much of their enormous search traffic is attributable to the excellent signals they send Google. They are the best in my opinion at meeting the standards set by Google’s Search Quality Evaluator Guidelines, a qualitative account of what Google’s search algorithms are looking for in a website that they want to promote.

Dotdash is not gaming the system. They are simply playing the game of making the best content and winning year after year; they now have 20 consecutive quarters of double-digit revenue growth.

As Vogel said in 2015, “There will always be a place in the universe for what we do. We provide real value to people, and that builds loyalty. So if we get this right, we're going to last for a long time.”

IAC Valuation

Dotdash Meredith: $3.6 billion

10x $.450 digital adjusted 2024 EBITDA - $1.54 long-term debt + $.25 billion cash + $.36 accounts receivable

Emerging and Other: $.967 Billion

1.5x 4*($161.1M revenue Q2 2022)

This is conservative as Vivian Health has a $400 million private market valuation and Care.com may be worth over $1 billion.

Search: $.312 Billion

3x operating income of $104 million (run rate first half 2022)

Conservative estimate of Turo Stake + value after warrant exercised: $1.2 billion

27% Turo stake + 10% warrant stake with exercise price ~2.35x more expensive than original stake price: $1.309 Billion

27% stake: 8 x 4*($142.85M revenue rr in Q1 2022)*.27 = $1.2 billion

10% warrant: 8 x 4*($142.85M revenue rr in Q1 2022)*.1 = 0.5 billion

- warrant exercise price: $250/.27*.1*2.35 = $0.2 billion

= $1.5 billion

Now to be on the safe side, let’s subtract 20% of the previous valuation of IAC’s Turo stake + warrant because Turo’s boost from pandemic reopening + car rent crunch is temporary.

$1.5 billion * 0.8 = $1.2 billion

Corporate drag: -$1.016 Billion

7x corporate expenses run rate Q2 2022

84.5% Angi Stake: $.887 Billion

$1.5 billion * .845 - 30% discount because I don’t have much conviction on Angi’s future prospects

16.5% MGM Stake: $1.95 Billion

$11.81 Billion * 16.5%

Cash on hand: $1.8 Billion

Debt: $0

IAC has no debt on its balance sheet. Dotdash Meredith has $1.6 billion in debt on its balance sheet. Angi has $500 billion in debt (hopefully) accounted for in its stock price.

IAC Valuation: $9.7 Billion

Current Market Cap: $4.83 Billion

Upside: 100%

Additional Thoughts

Close to the word limit, I do not have space to fully explain my bullishness on Turo. All I can say is this:

I believe that Turo has a better than fair shot at attaining cognitive referent status, entering a tier of only the most highly regarded brands. It has great economics, rapid growth, exceptional management, a high-energy and very positive culture, a mission that is highly persuasive, a remarkable NPS against competitors with some of the lowest NPS among all businesses, many guest and host evangelists, a strong moat that grows stronger by the day, a reasonably but not highly secure balance sheet, and a repeatable playbook that Uber and Airbnb pioneered to beat regulators and legislators. Furthermore, Turo is beginning to receive substantial free publicity in the media. When you put all of these characteristics together, regardless of what sector a company is in, I believe you have a valuable company.

As the named investor Nick Sleep once said, “The only real, long-term risk, is the risk of mis-analyzing a company's destination.”

Dotdash Meredith and Turo’s destinations appear likely to be remarkable. All though based on hand-wavy analysis, I can see each of them being $20 billion companies in a decade.

Buying Strategy Considerations

More than half of IAC’s market cap currently comes from its stakes in MGM and Angi. Until the value of Dotdash Meredith and Turo is uncovered in financial metrics (likely a few years from now), IAC’s stock price will likely be closely tied to the movements of $MGM and $ANGI.

IAC is exactly the kind of company the market doesn’t want right now. It is a high-growth company that does not report a profit in an inflationary environment with rapidly rising interest rates. Much of IAC’s current market valuation is tied to MGM and Angi, whose bonds are deemed non-investment grade. Recession fears are growing, exacerbating the likelihood that MGM and Angi valuations fall substantially, taking IAC down with them. Much of IAC’s portfolio is unproven VC-like binary bets (which are very much out of favor right now).

Few if any short-term catalysts.

Potential long-term Catalysts: 1) Dotdash Meredith spinning out — the likely next candidate, 2) Turo IPO — an IPO registration form was filed on January 10th, 2022, and an updated form was filed on May 20, 2022.

I recommend buying and holding IAC whenever you feel profitless US tech companies in general have nearly bottomed.